Pricing for Wills, Trusts & Probate

At IBB Law we like to, in very clear and simple terms, respond to the principal questions that clients have about working with a solicitor, namely;

- What are you going to do for me?

- What aren’t you doing for me?

- Who is going to do it?

- When will it be done by?

- How much is it going to cost?

In relation to our costs, we have a philosophy of ‘no surprises’. That puts the onus on us to address the questions above as transparently and as simply as possible.

As far as practicable, we also endeavour to provide clients with pricing choice. This recognises the fact that clients have different priorities and even the same client can have different pricing and payment priorities on different transactions or matters.

When we provide you with an estimate we will also provide you with a job specification that answers in clear and straightforward terms the questions above.

Set out below are some of the typical situations about which you may enquire and an estimate of the likely cost of our legal services. In the interests of giving you a clear and concise estimate we have made some assumptions about what you will need and provided you with a narrow range (within which the majority of our cases fall). We have included examples to help you see if the estimate is relevant to you. We have also included some of the most common factors which would increase or decrease our estimate.

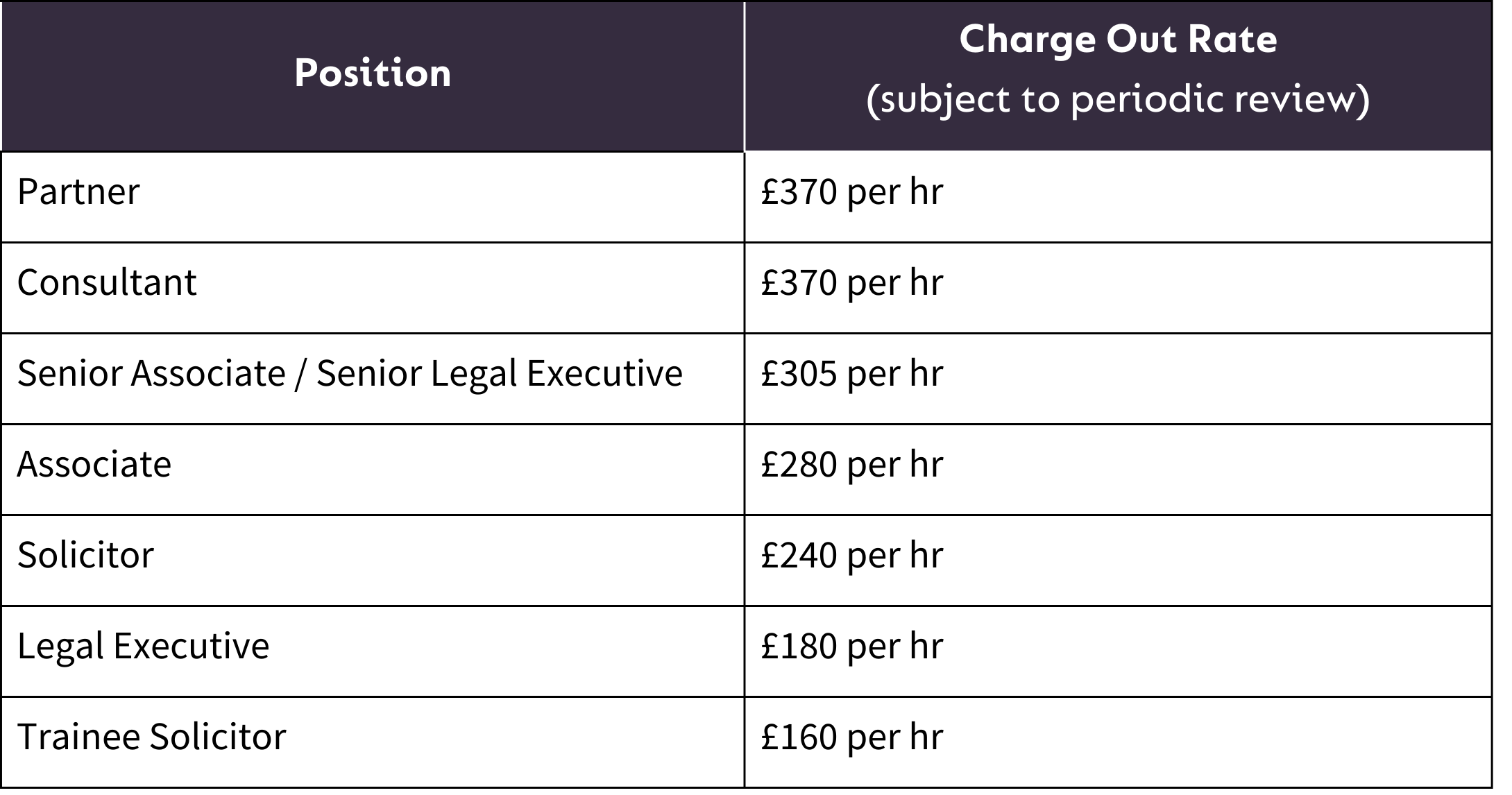

Our charges will normally be calculated by reference to hourly rates (as per the schedule below) agreed for the particular matter although we are prepared to consider alternative fee structures on a case-by-case basis.

All legal fees and disbursements incurred will be subject to applicable standard VAT at the prevailing rate (currently 20%).

Client Examples:

1. Taxable Estate

Details of a typical taxable estate:

- There is a valid Will.

- All of the assets of the estate are in the UK.

- There is only one property in the Estate which was the deceased’s residence.

- The remainder of the estate consists of bank/building society accounts and share-holdings/investment portfolios.

Scope: Summary of the work carried out in the administration of the Estate

(a) Interview with you to advise on the terms of the deceased’s Will and discuss the duties of the executors.

(b) Obtain valuations of the estate assets and liabilities. Write to utilities, council tax, house insurance and share registrars if applicable.

(c) Once the value of the assets has been received, prepare the Inheritance Tax form and ascertain the Inheritance Tax payable in the Estate

(d) Submit the Inheritance Tax to HMRC and arrange the first payment of Inheritance Tax from the assets of the estate

(e) Once the code is received from HMRC, prepare the legal statement and submit the application to the Probate Court to obtain the Grant of Probate.

(f) Send the Grant of Probate and letters of authority to the financial institutions, collect the assets in and pay any liabilities.

(g) Any correspondence with HMRC regarding the Inheritance Tax Account, in particular the property valuation, liaising with the District Valuer, ensuring the Inheritance Tax is discharged and obtain a clearance certificate from HMRC.

(h) Arrange Statutory notices for creditors in the London Gazette/Local magazines

(i) Correspond with beneficiaries regarding the distribution of the estate, pay any interim legacies or any pecuniary legacies that are due under the Will.

(j) Prepare Estate Accounts for executors.

(k) Bankruptcy checks for beneficiaries.

(l) Pay the final balance out.

Assumptions:

- There are no unusual funeral requests in the Will and the body is not being donated for medical research.

- The Executors are able/willing to act in the administration of the estate.

- We are able to speedily identify all assets and liabilities of the estate.

- There are sufficient assets in the estate directly accessible to fund any inheritance tax payable prior to obtaining the grant and a loan is not being applied for.

- There are no technical or other impediments to a Grant of Probate being issued by the Probate Court and the Will being proved as the last Will and Testament of the deceased.

- There are no claims against the estate by relatives, creditors or others and no caveats lodged at the Court.

- All beneficiaries reside in the UK and can be identified, traced and are at least 18 years of age and able to understand and sign documentation as required.

- There are no material disagreements amongst the beneficiaries and/or the trustees.

- The deceased’s property is their main residence and in good condition with no outstanding insurance claims.

- Buyers for the assets including the property are found and sales will complete within 6 months of the grant of probate being obtained.

- The property was not let at death or continues to be let during the estate administration.

- The will was validly executed and there is no partial intestacy.

- The estate is solvent.

- The deceased’s lifetime tax affairs are up to date.

Exclusions:

- The legal work relating to the sale of the deceased’s main house

- Any interest in property owned by the deceased outside the jurisdiction of England and Wales.

- Changes to legislation during course of estate administration.

- Trusts in which the deceased was a beneficiary at the date of death.

- Trusts set up by the deceased under the Will.

- Deeds of Variation for the beneficiaries.

- Financial advice on the suitability of the disposal of assets in the estate.

- Personal Taxation of estate beneficiaries.

- The sale of the deceased’s interest in a business or farm.

- Restitution for long term care funding incorrectly paid by the deceased.

- Income tax returns/tax declarations up to the date of death and during the administration period.

Who will do the work: In general this work will be done by one of the members of the team under the supervision of the partners in the team, Jacqueline Almond and Russell Hallam.

Price:

Our fees are based on our hourly rates and are estimated as follows:

- For the work carried out up to obtaining the Grant of Probate (steps (a) to (e) in the Scope of Work above): £2,500 – £4,000 plus VAT

- For work carried out post obtaining the Grant of Probate to finalising the administration of the Estate (steps (f) to (l) in the Scope of Work above) £3,000 – £4,000 plus VAT

Disbursements which may be incurred are:

- Valuation fees – approximately £200 plus VAT

- Land Registry fees – approximately £10

- Probate application – £300 plus £1.50 for each sealed copy

- Statutory Notices – £400

- Share sale charges – brokers fees including indemnity fees – dependent on the case and will include VAT

- Bankruptcy Search fees – £2 per beneficiary

Timescale:

- Typically obtaining the Grant of Probate takes 16-20 weeks

- Collecting in the majority of the assets (i.e. closing bank accounts and selling shares) generally takes up to 12 weeks after obtaining the Grant of Probate

After all the liabilities of the estate have been paid and any cash legacies distributed (provided we are not awaiting clearance from HMRC for either IHT or income tax) we are typically in a position to distribute the estate within 10-15 weeks of these matters being settled.

We would aim to complete the estate within twelve months of the date of death (or from when we are instructed if later); however this is subject to the assumptions set out above.

Increasing factors:

- The validity of the Will is disputed

- Disputes between beneficiaries on division of assets

- Caveats lodged at Court which prevent a Grant of Probate being

- Claims against the estate by relatives, creditors or others

- Life policies or pension arrangements to be dealt with as part of the administration of the estate

- The assets of the estate consist of a business or farm

Decreasing factors:

- Shareholdings are held within one investment portfolio.

- There is only one beneficiary of the estate and no cash gifts payable.

2. Non-taxable Estate

Details of a typical taxable estate:

- There is a valid Will.

- All of the assets of the estate are in the UK.

- There is only one property in the Estate which was the deceased’s residence.

- The remainder of the estate consists of bank/building society accounts and share-holdings/investment portfolios.

- Due to the value of the estate or the beneficiaries a full Inheritance Tax Account does not need to be submitted to HMRC

Scope: Summary of the work carried out in the administration of the Estate

(a) Interview with you to advise on the terms of the deceased’s Will and discuss the duties of the executors.

(b) Obtain valuations of the estate assets and liabilities. Write to utilities, council tax, house insurance and share registrars if applicable.

(c) Once the value of the assets has been received, prepare the Legal Statement (application for the Grant).

(d) Lodge the papers to obtain the Grant of Probate.

(e) Send the Grant of Probate and letters of authority to the financial institutions, collect the assets in and pay any liabilities.

(f) Arrange Statutory notices for creditors in the London Gazette/Local magazines

(g) Correspond with beneficiaries regarding the distribution of the estate, pay any interim legacies or any pecuniary legacies that are due under the Will.

(h) Prepare Estate Accounts for executors.

(i) Bankruptcy checks for beneficiaries.

(j) Pay the final balance out.

Assumptions:

- There are no unusual funeral requests in the Will and the body is not being donated for medical research.

- The Executors are able/willing to act in the administration of the estate.

- We are able to speedily identify all assets and liabilities of the estate.

- There are no technical or other impediments to a Grant of Probate being issued by the Probate Court and the Will being proved as the last Will and Testament of the deceased.

- There are no claims against the estate by relatives, creditors or others and no caveats lodged at the Court.

- All beneficiaries reside in the UK and can be identified, traced and are at least 18 years of age and able to understand and sign documentation as required.

- There are no material disagreements amongst the beneficiaries and/or the trustees.

- The deceased’s property is their main residence and in good condition with no outstanding insurance claims.

- Buyers for the assets including the property are found and sales will complete within 6 months of the grant of probate being obtained.

- The property was not let at death or continues to be let during the estate administration.

- The will was validly executed and there is no partial intestacy.

- The estate is solvent.

- The deceased’s lifetime tax affairs are up to date.

Exclusions:

- The legal work relating to the sale of the deceased’s main house

- Any interest in property owned by the deceased outside the jurisdiction of England and Wales.

- Changes to legislation during course of estate administration.

- Trusts in which the deceased was a beneficiary at the date of death.

- Trusts set up by the deceased under the Will.

- Deeds of Variation for the beneficiaries.

- Financial advice on the suitability of the disposal of assets in the estate.

- Personal Taxation of estate beneficiaries.

- The sale of the deceased’s interest in a business or farm.

- Restitution for long term care funding incorrectly paid by the deceased.

- Income tax returns/tax declarations to HMRC up to the date of death and during the administration period.

Who will do the work: In general this work will be done by one of the members of the team under the supervision of the partners in the team, Jacqueline Almond and Russell Hallam.

Price:

Our fees are based on our hourly rates and are estimated as follows:

- For the work carried out up to obtaining the Grant of Probate (steps (a) to (d) in the Scope of Work above): £2,000 – £3,000 plus VAT

- For work carried out post obtaining the Grant of Probate to finalising the administration of the Estate (steps (e) to (j) in the Scope of Work above): up to £3,000 plus VAT.

Disbursements which may be incurred are:

- Valuation fees – approximately £200 plus VAT

- Land Registry fees – approximately £10

- Probate application – £300 plus £1.50 for each sealed copy

- Statutory Notices – £400

- Share sale charges – brokers fees including indemnity fees – dependent on the case and will include VAT.

- Bankruptcy Search fees – £2 per beneficiary

Timescale:

- Typically obtaining the Grant of Probate takes 16-20 weeks

- Collecting in the majority of the assets (i.e. closing bank accounts and selling shares) generally takes up to 12 weeks after obtaining the Grant of Probate

- After all the liabilities of the estate have been paid and any cash legacies distributed (provided we are not awaiting clearance from HMRC for the estate’s income tax position) we are typically in a position to distribute the estate within 8-10 weeks of these matters being settled.

- We would aim to complete the estate within nine to twelve months of the date of death (or from when we are instructed if later); however this is subject to the assumptions set out above.

Increasing factors:

- The validity of the Will is disputed

- Disputes between beneficiaries on division of assets

- Caveats lodged at Court which prevent a Grant of Probate being

- Claims against the estate by relatives, creditors or others

- Life policies or pension arrangements to be dealt with as part of the administration of the estate

- The assets of the estate consist of a business or farm

Decreasing factors:

- The estate consists of jointly held assets which pass automatically to the surviving spouse.

- Shareholdings are held within one investment portfolio.

- There is only one beneficiary of the estate and no cash gifts payable.

Client Examples: Non-Taxable Estate

Details of a typical estate:

- There is a valid Will.

- The estate is solvent.

- All of the assets of the estate are in the UK.

- There is only one property in the Estate.

- The remainder of the estate consists of bank accounts and investment portfolios.

- All beneficiaries reside in the UK, can be traced and are at least 18 years of age.

- Due to the value of the estate or the beneficiaries of the estate,, there is no Inheritance Tax payable and a full Inheritance Tax Account does not need to be submitted to HMRC.

Scope: Summary of the work carried out in the administration of the Estate

(a) Interview with you to advise on the terms of the deceased’s Will and discuss the duties of the executors.

(b) Obtain valuations of the estate assets and liabilities. Write to utilities, council tax, house insurance and share registrars if applicable.

(c) Once the value of the assets has been received, prepare the Inheritance Tax form, Oath for Executors (application for the Grant) and ascertain the Inheritance Tax payable in the Estate

(d) Submit the Inheritance Tax to HMRC and arrange the first payment of Inheritance Tax from the assets of the estate

(e) Once the IHT receipt is received from HMRC, submit the application to the Probate Court and lodge the papers to obtain the Grant of Probate.

(f) Send the Grant of Probate and letters of authority to the financial institutions, collect the assets in and pay any liabilities.

(g) Any correspondence with HMRC regarding the Inheritance Tax Account, in particular the property valuation, liaising with the District Valuer, ensuring the Inheritance Tax is discharged and obtain a clearance certificate from HMRC.

(h) Arrange Statutory notices for creditors in the London Gazette/Local magazines

(i) Correspond with beneficiaries regarding the distribution of the estate, pay any interim legacies or any pecuniary legacies that are due under the Will.

(j) Prepare Estate Accounts for executors.

(k) Bankruptcy checks for beneficiaries.

(l) Pay the final balance out.

Exclusions:

- Tax Returns to the date of death or during the administration Period

- Deeds of Variation

- Conveyancing work in relation to the sale of the property

Who will do the work: In general this work will be done by one of the members of the team under the supervision of Jacqueline Almond.

Price:

Our fees are based on our hourly rates and are estimated as follows:

- For the work carried out during the administration period up to obtaining the Grant of Probate (i.e. steps (a) to (d) above: £2,500 – £4,000 plus VAT

- For work carried out post obtaining the Grant of Probate to finalising the administration of the Estate (i.e. steps (e) to (l) above): £3,000 – £4,000 plus VAT

Disbursements which may be incurred are:

- Valuation fees – approximately £200 plus VAT

- Land Registry fees – approximately £10

- Probate application – £273 plus £1.50 for each sealed copy

- Statutory Notices – £400

- Share sale charges – brokers fees including indemnity fees – dependent on the case and will include VAT.

- Bankruptcy Search fees – £2 per beneficiary

Increasing factors:

- The validity of the Will is disputed

- Disputes between beneficiaries on division of assets

- Caveats lodged at Court which prevent a Grant of Probate being

- Claims against the estate by relatives, creditors or others

- Life policies or pension arrangements to be dealt with as part of the administration of the estate

- Beneficiaries reside outside of the UK

- There are assets outside of the UK and probate (or the foreign equivalent) needs to be obtained in this jurisdiction.

Every client is individual and has specific needs. Having taken a look at these examples, if you are happy to speak to us further, please give us a call or drop us an e-mail. We will be happy to answer any questions or provide clarification. We will almost certainly need additional information to give you the most certain estimate, and we can discuss any issues of urgency or particular circumstances that you think we ought to know. Once the details are settled, we will send out normal client care and engagement documentation and you can decide whether you are happy to proceed.

Meet the team

-

-

- Colin Glass

- Consultant

-

-

-

- Jane Beaven TEP

- Senior Associate

-

-

-

- Linda Blay TEP

- Senior Associate

-

-

-

- Elena Hall TEP

- Chartered Legal Executive

-

-

-

- Muna Ahmed

- Legal Administrator

-

-

-

- Maryam Dean

- Trainee Solicitor

-